You Happen To Money, It Doesn’t Happen To You

That little shower thought from last blog got me thinking about another side to that same coin, a more active role as the emphasis is that you actually have to do what you have to do (unfortunately…). This is also a thread which is woven through everything good in my life.

Stop letting money happen to you (And start happening to it)

This is related to a habit I developed right at the beginning of my personal finance journey so, getting on for 8 years ago or so. I call it ‘sorting out my finances’. It’s developed over the years but there’s a consistency to it:

I write down, on paper, what goes in and out of my bank account every week.

That’s changed over time as I invested more, started doubling down on using cashback credit cards, me and Dr Chris changed how we split bills and how we paid for them (jointly or by paying each other back). It’s changed now I’m in Sweden and spending a lot less, I still work in weeks but I don’t need to actually sit and do it so often.

This Isn’t A Budget How-To

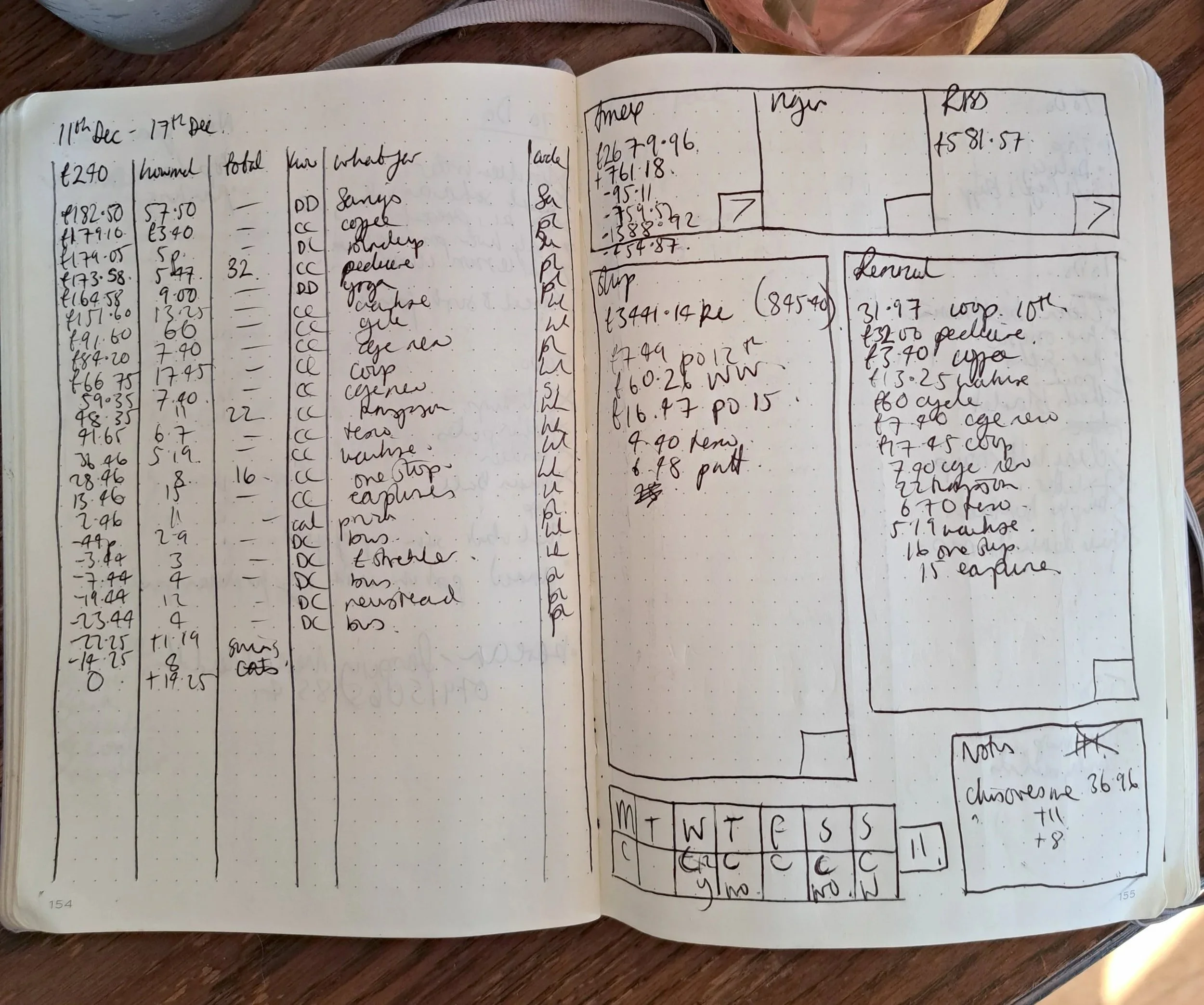

This method is really personal. Like seriously personal. I once showed it to an accountant friend of mine and his mind was blown. As I explained it, he understood it was a form of sort of zero-based budgeting - but with stuff all over the place, links to different blocks of info, notes and codes - it looks like nowt on God’s earth.

A page from a few years ago. I understand every single thing on here and I would bet a lot of money that nobody else does!

It also doesn’t make for easy oversight, so it’s not something I could use for the 50/30/20 method or even use towards the net worth workings out - it’s also not an equivalent to some of the much more efficient budgeting maps I have to help clients (when HMRC finally gives me the go-ahead… come on guys!).

But it does have purpose, the main one being that it was the first time that I ‘happened to’ money. I’d followed budgets before, I’d done what I was supposed to do, but it never stuck because it didn’t work in my brain. Not only was money happening to me, but these methods of dealing with it were also happening to me - and if there’s one thing about me, it’s that I’m gonna resist being told what to do if it doesn’t make sense.

Other purposes it served over time:

It was a check in on every single item and service - a spark-joy-check before I’d read the book I suppose.

If I avoided doing it I knew I was anxious. Maybe about money, but often about other stuff.

Over time I found I could use it to get me out of an anxiety hole because stuff was mostly better than my brain told me it was, and if it wasn’t, I always dealt with it and that gave me proof that I could always deal with it.

What You Can Take From This

Once you are happening to money, instead of it happening to you, then my goodness your options open up. It allows you to poke around a bit, make some decisions, begin to use money as a tool for the life you want instead of it simply limiting the life you’re in now.

That’s quite exciting!

Love Eleanor. xxx