Compound Interest

Compound interest as a concept will be something we come back to again and again (it’s relevant in the 4% rule for example) so I really want to cover it well. It’s the first real finance thing I spoke about on the Instagram and Facebook and I think it’s just such an exciting concept - even if it might feel a little mathsy…

Compound interest is the secret sauce which means that time, rather than the amount you invest, is often the important factor in wealth creation.

By mentioning time, I don’t want that to stress you out with thoughts about what you could have done - I want it to inspire you to do something today! Because in ten years time, ten years will have passed whether you did the thing or not, you might as well be benefiting from the compounding effects.

Okay - the good stuff:

Compound interest means earning interest on your interest – it’s a snowball effect.

Compare it with simple interest where you only earn money on your initial investment, so 10% interest on £1000 investment:

Year one: £1,100.

Year two: £1,200.

Year three: £1,300.

…

Year ten: £2,000.

Compound interest, 10% on a £1,000 investment but importantly also on your interest:

Year one: £1,100 (same!).

Year two: £1,210.

Year three: £1,331.

…

Year ten: £2593.74.

That’s cool yeah? Now, there’s nothing particular you need to do for compound interest - it’s not a special offer or package or anything. It’s the effect of putting your interest back into the same account and leaving it be. It’s vanishingly rare for banks to offer simple interest so it’s likely you’re already benefitting without realising!

You can absolutely smash compound interest through the roof if…

you pair it with regular saving too - your savings will grow exponentially!

So, if we take the figures from before, £1,000 initial investment, 10% interest rate, compounded yearly over 10 years. How does it look if you leave it alone, compared to if you add £100 a month?

The final totals would be: £2,594 vs £22,595.

And the actual interest accrued would be: £1,594 vs £9,595.

How about you increase that £100 you’re investing by 10% each year as you get promotions etc. (so £100 in the first year, £110 in the second year, £121 in the third year)? That looks like £32,187 which include interest of £12,061.

These are some serious numbers, ey?! I couldn’t work this out on my own by the way, I’m no maths genius, I just love to fanny about on this compound interest calculator.

We’ve focussed in on the exciting stuff but it’s worth noting that this applies to loan interest and inflation too. An awareness of how it functions could mean the difference between either benefitting from compound interest or paying to a credit card company.

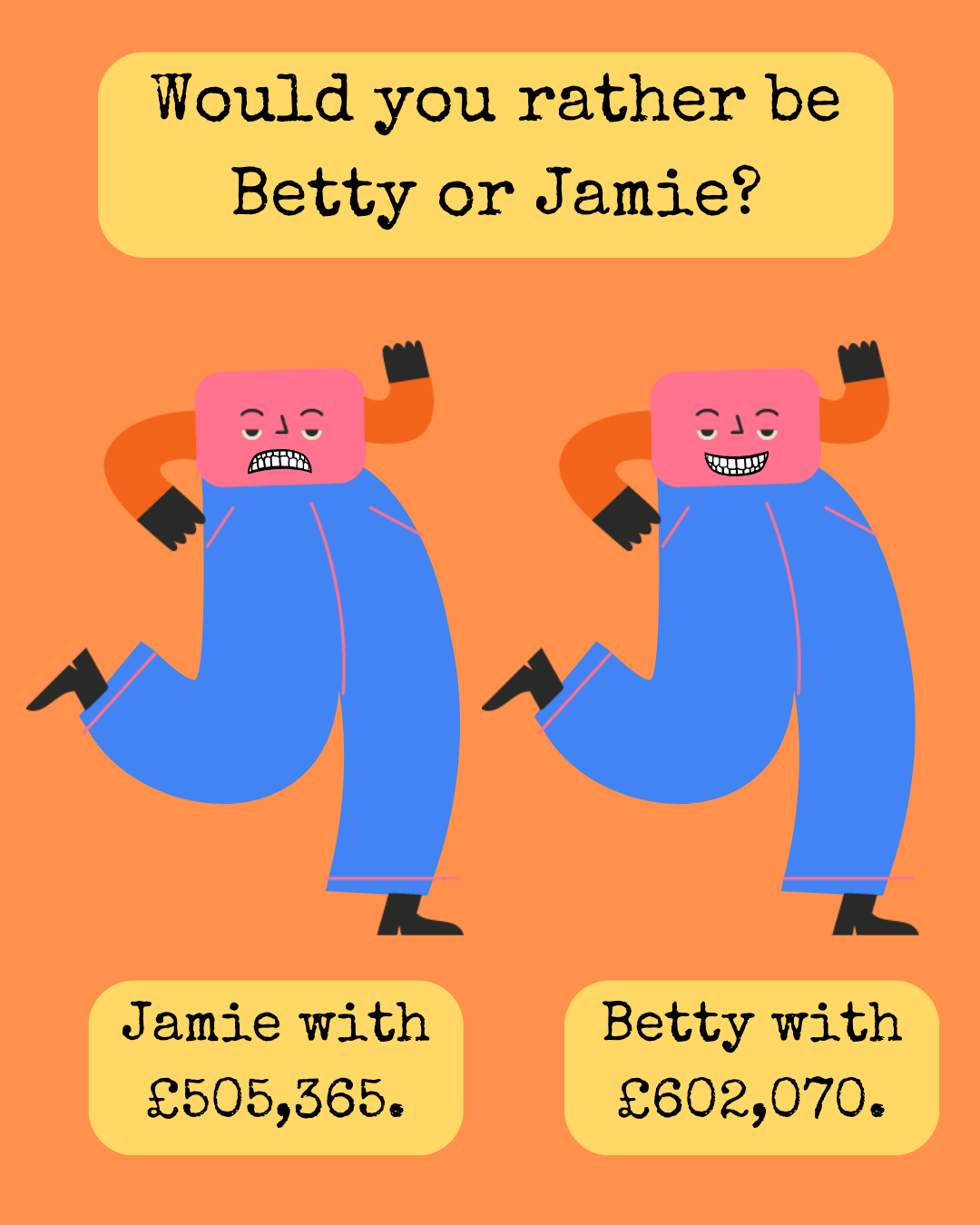

I want to finish up with a real gem for you which I think perfectly encapsulates how important this concept is. It regards two people, I’ve called them Jamie and Betty.

Betty invests £5,000 a year from age 25-35 (so £50,000 in total).

Jamie invests £5,000 a year from 35-65 (so £150,000 in total).

At age 65, assuming 7% returns (which is fairly standard in the stock market):

Betty ended up with more, even though they invested a third of what Jamie did, because she started earlier and let time do the work.

But again, I tell you this not to stress you out but to suggest that you do as Betty did and make some money moves!

Have you ever thought so much about interest? 🤯

Love Eleanor. xxx

P.s. I answered some questions which came up from this blog right here.